Bitcoin vs. CBDCs: The Battle for Financial Freedom

In the 21st century, money isn’t just a tool—it’s a weapon. And right now, a silent war is being fought between two radically different visions for the future of finance: Bitcoin and Central Bank Digital Currencies (CBDCs).

In the 21st century, money isn’t just a tool, it’s a weapon.

And right now, a silent war is being fought between two radically different visions for the future of finance: Bitcoin and Central Bank Digital Currencies (CBDCs).

One is open, decentralized, and borderless.

The other is programmable, centralized, and tightly controlled.

Only one truly protects your financial freedom.

Bitcoin: The Money of the People

Bitcoin was born out of rebellion.

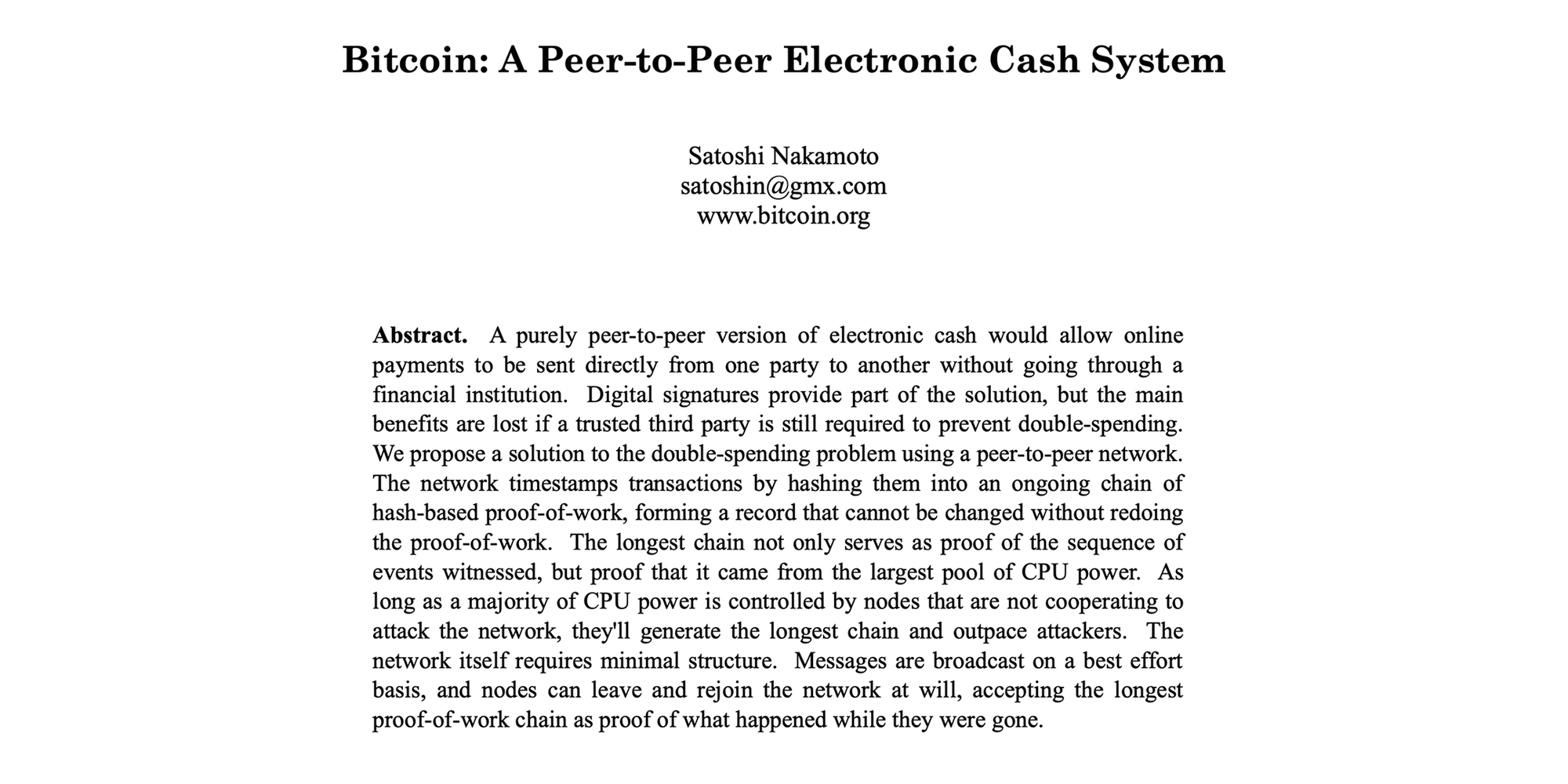

In 2009, while banks were being bailed out and trust in financial institutions crumbled, an anonymous coder named Satoshi Nakamoto released Bitcoin as a lifeline, a peer-to-peer form of money that doesn’t need permission or intermediaries.

Bitcoin is:

- Decentralized: No government or corporation can alter its supply or transactions.

- Transparent: Every transaction is recorded on a public blockchain.

- Scarce: Only 21 million will ever exist—no inflation, no printing, no bailouts.

- Borderless: It moves freely across countries, banks, and regimes.

Bitcoin gives individuals financial sovereignty, the power to hold and transfer value without gatekeepers.

CBDCs: The Digital Cage

CBDCs (Central Bank Digital Currencies) are the state’s response to Bitcoin’s rise.

Governments see Bitcoin’s success and want in, but on their terms.

Unlike Bitcoin, a CBDC isn’t money you own.

It’s money you rent from the state, fully programmable, trackable, and revocable.

Imagine a system where:

- Every transaction is monitored in real time.

- Your spending can be restricted or reversed.

- Expiration dates can be placed on your money.

- “Social credit” can influence your access to funds.

CBDCs are digital fiat with total surveillance built in.

Lots of potential misuse of CBDC features:

- Surveillance and loss of privacy: A fully trackable CBDC could allow central banks and governments access to detailed, real-time transaction data. This raises significant concerns about state-level surveillance and the potential for abuse of personal information for purposes beyond its initial collection.

- Programmable money and control: The programmable nature of a CBDC could enable the government to control and restrict how individuals use their money. This could include setting expiration dates on funds, limiting purchases of certain products, or imposing spending caps.

- Revocable money: While not as widely discussed as programmability and tracking, the concept of a revocable CBDC introduces the risk of central authorities freezing or reducing user funds. This gives the state extraordinary financial control over its citizens and could lead to unfair or discriminatory actions.

- Political censorship: The potential for a CBDC to be used for political control and punishment is another serious risk. The government could block transactions based on the political activities or beliefs of individuals or groups, penalizing those deemed undesirable.

- Risk to civil liberties: Overall, these features threaten civil liberties by enabling increased state power over individuals' economic lives. This is especially concerning in countries with weak rule of law, where robust institutional safeguards are not guaranteed to prevent the abuse of these capabilities.

- Cybersecurity risks: A centralized CBDC system would be a high-value target for cyberattacks by criminals and hostile nation-states. Any breach could compromise sensitive user data and lead to financial fraud and loss of public trust.

- Exclusion of vulnerable populations: The reliance on digital infrastructure for a CBDC could exclude vulnerable groups, such as the elderly, homeless, or those without access to technology, particularly if cash were to be phased out.

They offer convenience at the cost of total control.

The Clash Ahead

The fight between Bitcoin and CBDCs isn’t technical, it’s ideological.

It’s about who controls the future of money: the people or the state.

- Bitcoin empowers individuals.

- CBDCs empower governments.

- Bitcoin is voluntary.

- CBDCs are mandatory.

- Bitcoin is freedom.

- CBDCs are control.

Governments will sell CBDCs as innovation, faster payments, safer money, better policy tools.

But the true purpose is centralized oversight.

Bitcoin, meanwhile, continues to evolve as a parallel system, a global, censorship-resistant alternative that thrives outside of their reach.

Choose Your Side

The choice isn’t coming... it’s already here.

As nations roll out pilot programs and CBDCs quietly integrate into payment systems,

Bitcoin stands as the last open-source monetary firewall.

In the coming years, every citizen, investor, and entrepreneur will face this question:

Do you want money that’s yours—or money that can be switched off?

Bitcoin represents the digital frontier of freedom.

CBDCs represent the digital prison of control.

History will remember which one you chose.

Buy & Sell Bitcoin, Dollar Cost Average management and pay your bills with Bitcoin on the the best Bitcoin only Exchange.

Comments ()