How Banks Create Money, and Why It Ends Up in Houses Instead of Innovation

If you want to understand why housing prices exploded, why wages feel stuck, and why the economy seems to get more fragile each decade, start with this simple fact: banks create most of the money in our economy out of thin air.

Not governments.

Not central banks.

Commercial banks.

And once you understand how they create it, you’ll see why so much of that new money gets pumped into the one thing that makes everyday life more expensive for everyone: real estate.

Buy & Sell Bitcoin, Dollar Cost Average management abd pay your bills with Bitcoin on the the best Bitcoin only Exchange.

The Hidden Engine: Fractional Reserve Money Creation

When you walk into a bank and ask for a mortgage, something surprising happens. The bank does not take deposits from other customers and hand them to you.

Instead, it creates a brand new digital IOU, credits your account, and calls it a mortgage loan.

That loan becomes new money inside the banking system.

This is the core of modern money creation:

- You sign for a loan.

- The bank creates new deposit money with keystrokes.

- That money enters the economy when you spend it.

Over 90 percent of the money supply originates this way. Banks do not lend existing money, they manufacture new purchasing power.

This system rewards banks for issuing as many safe, profitable loans as possible. Which leads to the big question: what is the safest, most profitable thing banks love to lend against?

Not new businesses.

Not innovation.

Not factories or productive assets.

The answer is simple: houses.

Why Banks Prefer Houses Over Innovation

Banks are not engines of economic creativity.

They are risk managers.

Their mission is to maximize return while minimizing the chance of a loan going bad.

A startup might 10x your investment, but it might also go to zero.

From a bank’s perspective, it is basically radioactive.

Housing, on the other hand, checks every box:

• Collateral they can seize if you miss payments

• Reliable demand especially when populations grow

• Predictable cashflows from interest

• Government support through policies, guarantees, and subsidies

• Low regulatory risk because the entire economy is built on housing stability

So banks push their newly created money into mortgages because mortgages are easy, low risk, and highly profitable.

This is why you’ve never heard of a bank officer begging you to take out a loan to build a robotics lab, a geothermal plant, or a new manufacturing shop.

But you’ve definitely seen banks cheerfully offering you a mortgage.

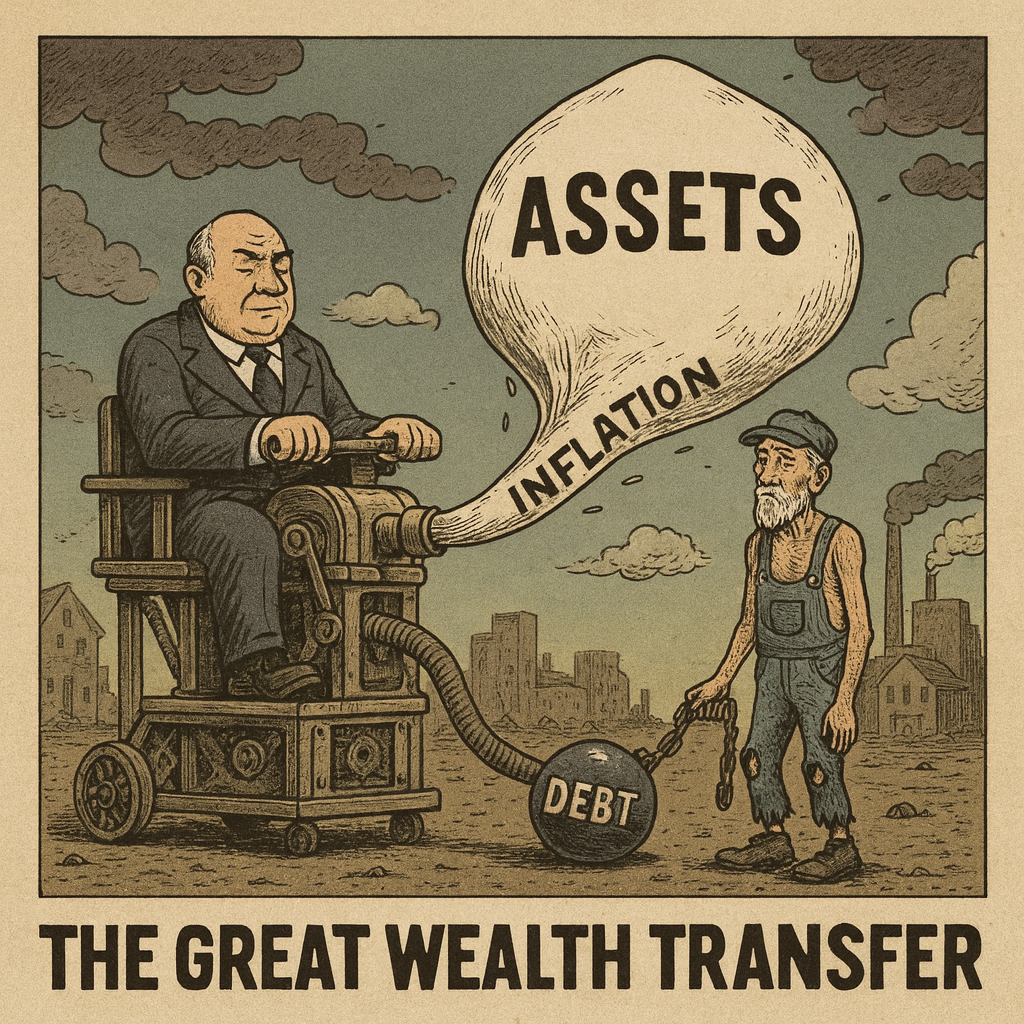

Asset Inflation vs Productive Growth

Once you realize that new money goes mostly into existing houses rather than new production, everything becomes clear.

You get:

• Higher home prices

• Stagnant wages

• No growth in productive capacity

• Boom and bust cycles

• A widening wealth gap

Money creation aimed at existing assets inflates asset values, not productivity.

So the economy becomes a giant balloon pressed upward by credit, without producing more goods or better technology underneath.

The rich get richer because they own the inflating assets.

Everyone else pays more for the same roof over their head.

Why Factories Don’t Get Built

To build a factory, you need long-term capital, patience, engineering talent, customers, and innovation. A bank sees that and thinks: risk.

A mortgage?

A house in a city with growing demand?

Guaranteed.

Safe.

Backed by the government.

Collateral you can grab in 60 days if needed.

So the banking system funds consumption and speculation rather than production.

This is why:

• We get more condos than machine shops

• We get rising home prices instead of rising manufacturing capacity

• We import more goods each year instead of producing them

• Our infrastructure ages while asset prices moon

The economy tilts toward whatever banks can easily lend against. And that means housing.

Why This Matters for the Future

When money creation is tied to housing credit, the economy becomes addicted to rising home prices.

Governments then intervene to protect that system at all costs, because if home prices fall, the entire banking sector wobbles.

This creates a cycle of:

• More credit

• Higher home prices

• More debt

• Less productive investment

• Slower real growth

It is a loop with no natural end.

Until something breaks.

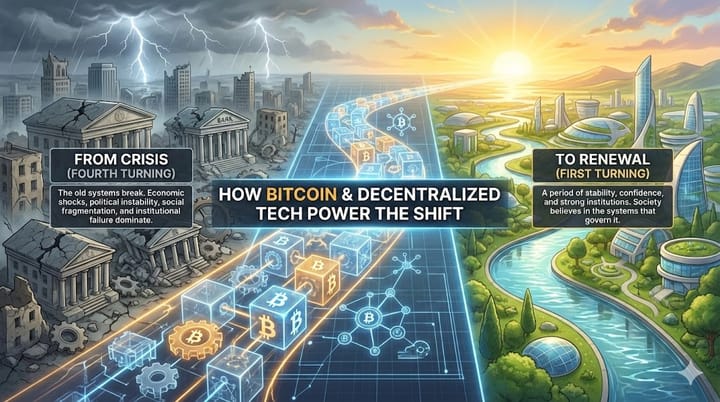

Bitcoin as a Breakaway System

Bitcoin flips this model on its head. It separates money creation from private banking and political incentives.

There is no central authority that can inflate the supply.

There is no credit creation based on collateral.

There is no advantage to pumping money into existing assets.

You either have Bitcoin or you do not.

No one can conjure it with keystrokes.

This creates an environment where capital must be used intentionally. You cannot simply borrow into existence and hope an asset’s price rises faster than your debt.

A sound money system forces real productivity, real value creation, and real innovation.

Your Bitcoin, your rules.

Buy it, sell it, hold it, spend it, and get it delivered straight to your wallet in minutes. Pay bills with Bitcoin and never rely on a custodial middleman again. Step into self-custody with Bitcoin Well.

The Bottom Line

Banks create money, but not for the purpose of building a better economy.

They create money wherever it is most profitable and least risky for them.

That usually means piling new credit onto the same houses, again and again, pushing prices up while the real economy stagnates.

Understanding this explains:

• Why home prices explode

• Why wages lag

• Why innovation slows

• Why inequality grows

And it also explains why a parallel system like Bitcoin is becoming essential for anyone who wants money that cannot be inflated away by private credit.

Comments ()