Unlocking Liquidity Without Selling: How Bitcoin-Backed Lending on Firefish Changes the Game

If you’re reading this on On Bitcoin, you already believe in the long-term value of holding bitcoin (BTC).

But what if you could use your bitcoin as collateral—getting access to fiat or stablecoin liquidity—without selling and losing your bitcoin exposure?

That’s exactly what Firefish offers: a Bitcoin-native lending marketplace built on transparency, open price discovery and non-custodial infrastructure.

Let’s dig into what this means, how it works, why it matters, and what to watch out for.

ON BITCOIN is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Why this matters: Borrowing from your bitcoin stack

Traditionally, if you held bitcoin and you needed cash (for life expenses, investment opportunities, taxes, or whatever), you had two main choices:

- Sell some of your bitcoin → triggers a taxable event, you reduce your stack, you lose optionality.

- Do nothing / borrow via traditional credit → may involve credit checks, high interest, or you dilute your bitcoin bet.

Platforms like Firefish allow you to access liquidity while keeping your bitcoin position intact.

The thesis: bitcoin is the ultimate collateral. Firefish puts this into practice.

Here are a few headline advantages:

- Keep your bitcoin exposure — you don’t sell, you borrow. On Firefish: “Borrow cash. Keep your Bitcoin.”

- Non-custodial collateral — your bitcoin isn’t handed over to a trusting third-party; it’s locked in on-chain, multi-sig escrow.

- Open marketplace pricing — borrowers set terms and lenders pick deals; more competitive than many centralized models.

- Stablecoin/fiat settlement options and global reach — e.g., USDC loans now available in 50+ countries.

From a strategy standpoint: If you’re bullish on bitcoin but need liquidity, you can use it as capital instead of disposing of it.

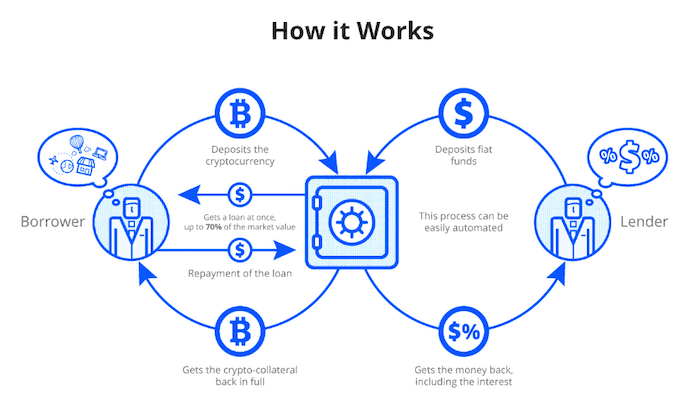

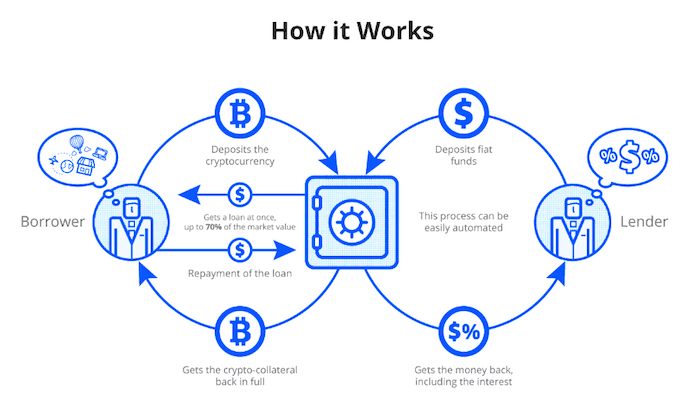

How Firefish works: A step-by-step breakdown

Here’s a simplified walkthrough of the borrower side of the platform.

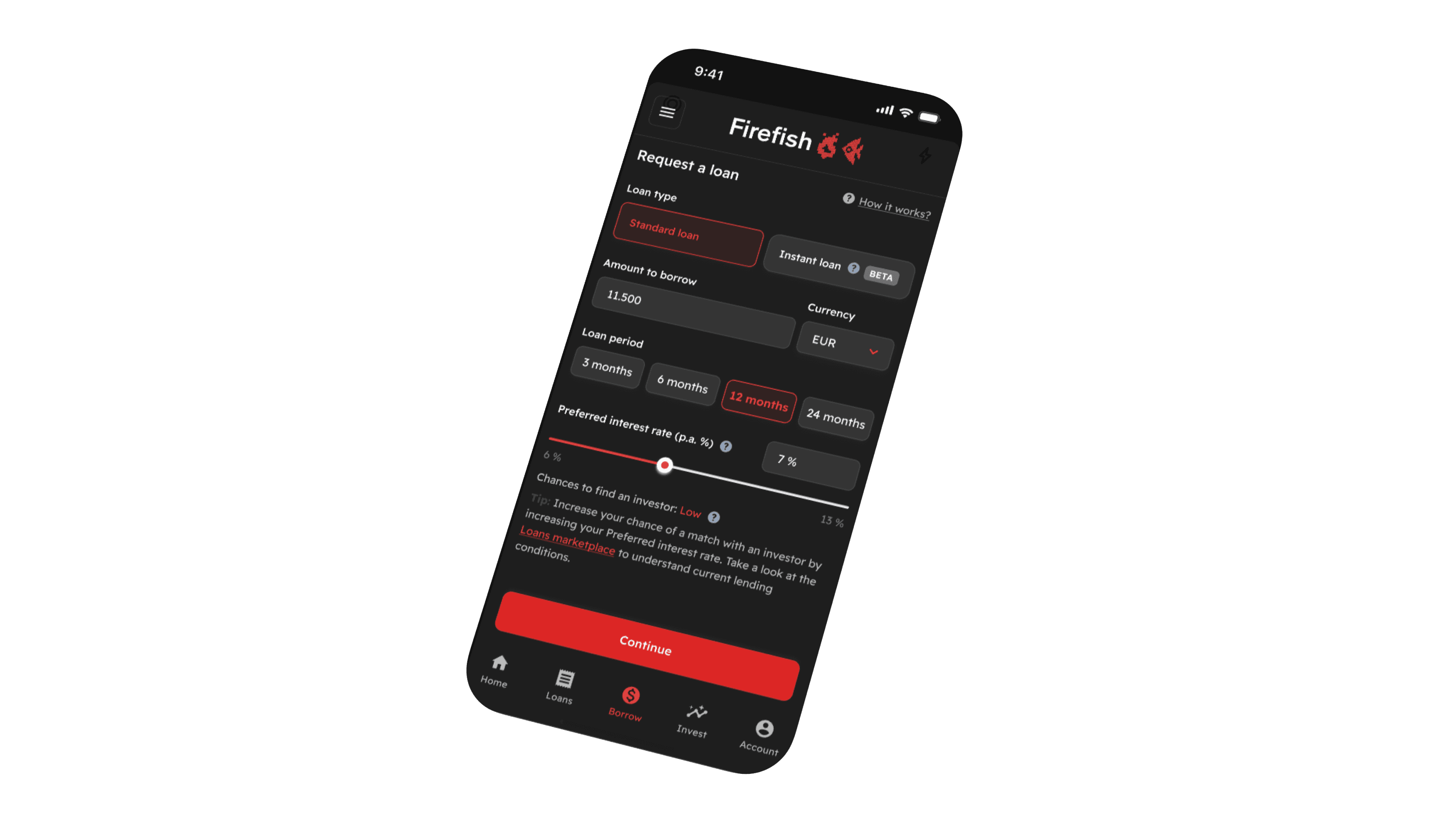

1. Define the loan terms

You go into the platform and specify: how much you want to borrow, in which currency (EUR, CHF, USDC, etc.), at what interest rate, and for how long (typically 3–24 months) according to Firefish’s current terms.

2. Match with a lender

Once you list your loan request, the marketplace finds a lender who accepts your terms (or you can select an instant-loan path with predefined terms).

3. Collateralize your bitcoin

You send your bitcoin (BTC) into a multi-signature on-chain escrow address.

At this point, you retain control of your keys but the collateral is locked in accordance with the contract.

Firefish emphasises “Secure, non-custodial escrow.”

4. Receive funds

Upon collateral confirmation, funds are transferred to you in fiat or stablecoin.

You then use your cash as you wish, while your BTC remains locked as security.

5. At loan maturity / early repayment

At the end of the term, you repay the principal plus interest.

Your bitcoin collateral is released back to you. You may also be able to repay early if the contract allows.

6. Liquidation risk

Because bitcoin is volatile, Firefish uses over-collateralisation (loan-to-value, or LTV around 50%) and has liquidation mechanisms if collateral value falls too far.

Key metrics & recent updates

- Firefish closed a $1.8 million seed round in early 2025, backed by prominent bitcoin-native investors such as Braiins.

- As of April-May 2025: over 10,000 users, nearly 1,000 BTC in escrow collateral, and cumulative loan volume exceeding $100 million.

- Instant loan option: USDC loans now available globally, with funding in as little as ~15 minutes according to Firefish.

- Interest rates for borrowers start around ~5-6% depending on terms and LTV.

- For investors (lenders), advertised returns “up to ~15% p.a.” for bitcoin-backed loans.

Why Firefish stands out (and what to appreciate)

Non-custodial collateral

One of the biggest risks in crypto lending is custodial risk: you hand over assets and lose control.

Firefish uses multi-sig on-chain escrow and claims no rehypothecation of collateral.

Marketplace transparency

Rather than a monolithic lender setting opaque rates, Firefish’s marketplace format allows borrowers to propose terms and lenders to choose, which fosters competition and transparency.

Bitcoin native, fiat/USDC settlement

For bitcoin-maximalist use-cases, you can stay long BTC while using it as collateral for liquidity in fiat or stablecoins.

This aligns with the stacking ethos.

Institutional scale & backing

With partners like Braiins backing the platform, and infrastructure designed for institutional involvement (e.g., “Firefish Prime”), the platform aims to bridge long-term bitcoin vision with serious capital.

Things to watch & caveats

- Liquidation risk – If bitcoin’s value falls sharply, the LTV may breach thresholds and collateral could be liquidated. Though Firefish uses a more conservative ~50% LTV, volatility remains a risk.

- Regulatory & jurisdictional issues – Borrowing fiat across borders or accessing stablecoins may involve KYC/AML, local banking limitations, or regulatory uncertainty.

- Counterparty / platform risk – While Firefish pledges no rehypothecation and non-custody, partake that this is still a relatively young platform (founded ~2022) and risk exists.

- Interest & terms change – The dynamic nature of interest rates and market-driven pricing means terms may shift. Always review carefully.

- Tax implications – While you’re not selling your BTC, borrowing against it still has tax considerations in many jurisdictions (interest payments, loan defaults, etc.). Consult your tax advisor.

- Liquidity of the loan market – Even though Firefish aims to be peer-to-peer, sufficient lender/investor liquidity is necessary for optimal terms and seamless matches.

Use-cases where Firefish makes strategic sense

- You believe bitcoin will appreciate long-term, yet you need short-to-medium term cash (say for investment, living expenses, taxes) and you don’t want to sell.

- You’re a business (e.g., a bitcoin miner) generating revenue in bitcoin but incur costs in fiat and want a way to convert exposure into working capital without liquidation.

- You’re an investor seeking yield in a world of low fixed-income returns and you’re comfortable with bitcoin-collateralised risk.

- You’re building a “long bitcoin, short fiat” strategy – use your bitcoin as a collateral vehicle so you can participate in fiat-based opportunities while retaining your bitcoin exposure.

My take: Where this fits in the Bitcoin stack

In the broader architecture of bitcoin finance, borrowing against your bitcoin is a critical component.

It lets you unlock value without giving up exposure. Platforms like Firefish accelerate the shift of bitcoin from simply a store of value to collateralizable capital.

I see this as the next frontier of “stacking sats”.

Instead of just accumulating bitcoin and waiting for price appreciation, you can activate your stack—use it to generate fiat liquidity, invest, trade, or build—while still being long.

However—and this is important—it’s not risk-free.

The volatility of bitcoin, the operational risks of new platforms, and the regulatory uncertainty mean this strategy must be executed with full awareness.

Don’t treat it like a savings account.

Treat it like leverage on your conviction, with all the attendant risks.

Final thoughts

Borrowing against your bitcoin (instead of selling) is a paradigm shift.

It takes the concept of “sound money” one step further toward “sound capital”.

With Firefish, you have a viable, Bitcoin-native pathway to liquidity: non-custodial, peer-to-peer, global.

It’s not perfect, but it’s one of the best options currently available.

If you’re interested, I’d recommend:

- Starting with a small “test” loan or investment to get comfortable with the mechanics.

- Carefully tracking your LTV and margin-call thresholds.

- Reading the documentation and understanding the contractual terms (collateral, liquidation triggers, recovery mechanisms).

- Keeping an eye on regulatory developments in your jurisdiction—especially around stablecoins and collateralised loans.

- Using this as part of a broader strategy—not as your entire bitcoin thesis.

👇 Coming Next: The Investor’s Perspective on Firefish

In the next article, we’ll dive deeper into how lenders earn yield on Firefish, how risk is managed, and what the true mechanics of Bitcoin-backed yield look like behind the scenes.

We’ll explore:

- How Firefish structures interest rates and loan terms.

- What happens if collateral gets liquidated.

- How lenders manage risk and generate consistent returns.

- How Firefish compares to other yield-earning options in Bitcoin finance.

Subscribe to On Bitcoin to get notified when the follow-up post drops — and learn how to put your bitcoin to work without selling it.

Comments ()